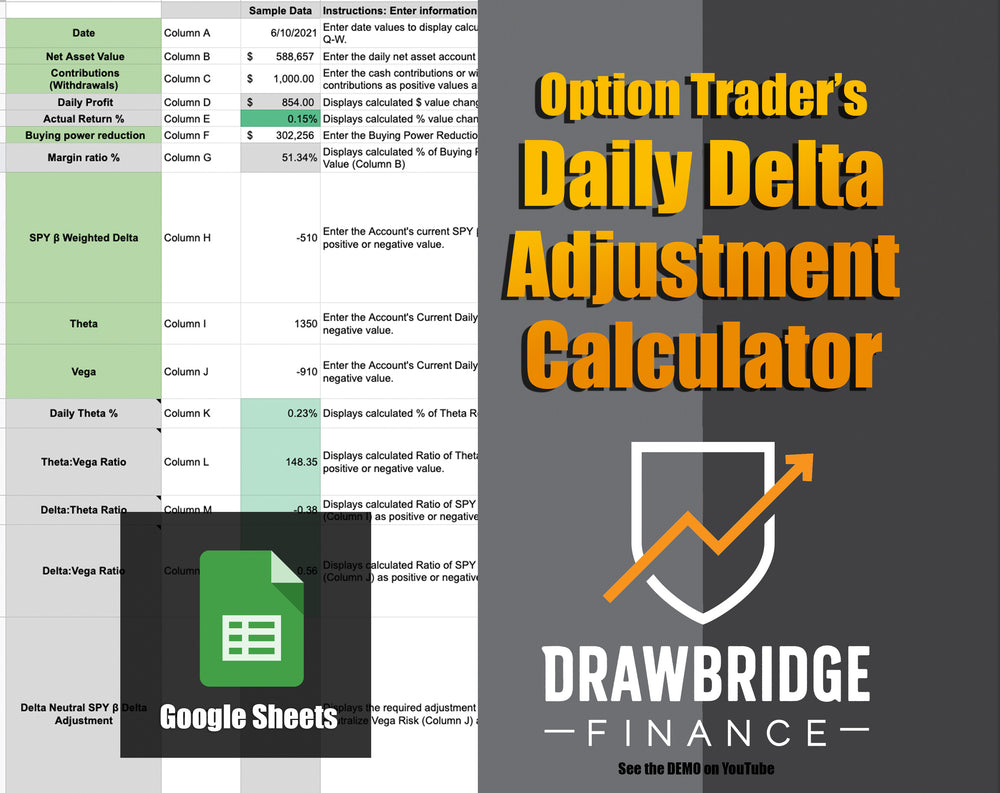

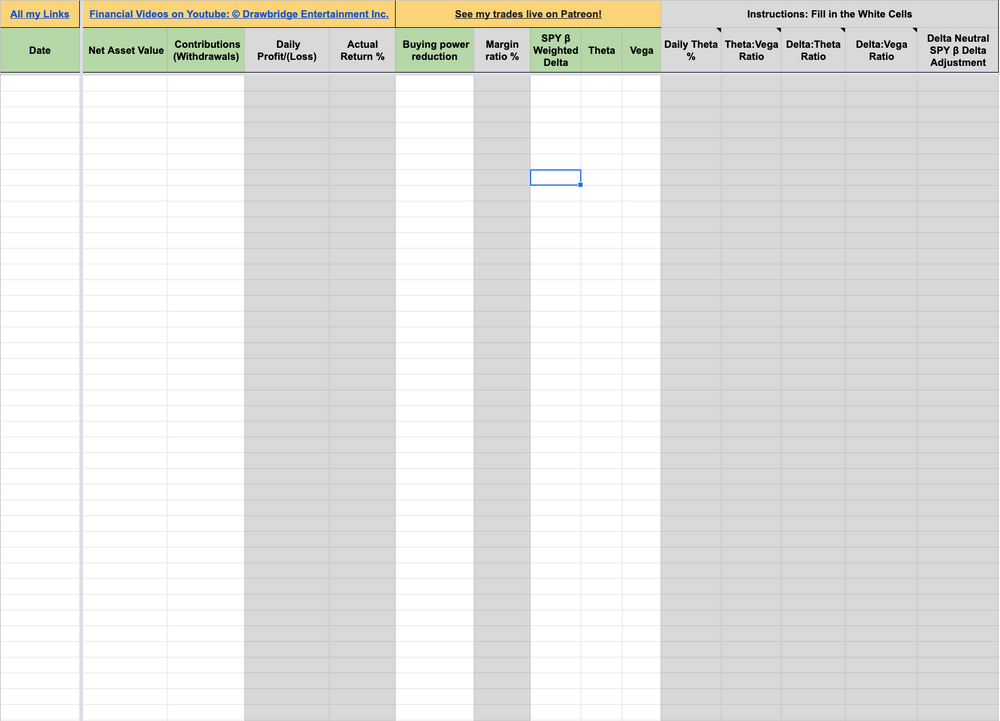

Option Traders Daily SPY β Delta Adjustment Calculator

Spreadsheet to calculate the required SPY β Delta Adjustment Required to neutralize the Vega risk in a portfolio

*** Digital Download: Google Sheets ***

This chart is ideal for investors that want to track a long term investment portfolio and the daily theta, delta and vega so that the portfolio can have a neutral outlook including an offset for the volatility risk created by holding short options.

This spreadsheet tracks account value, contributions/withdrawals, Buying power reduction, SPY β Weighted Deltas, Vega and Theta to calculate:

Daily Profit/(Loss)

Daily % Account Change

Margin Ratio %

Daily Theta Decay %

Theta:Vega Ratio

Delta:Theta Ratio

Delta:Vega Ratio

Delta Neutral SPY β Adjustment

All the result have coloured outputs based on customizable ideal ranges.

It also tracks and charts:

Monthly/Annual Summary

Contributions/Withdrawals

Monthly $ Change

Monthly % Change

YTD Running P/L

YTD Change

Number of up and down days

Daily Average $ Return

Daily Average % Return

The spreadsheet has 2 sheets:

• Annual Daily Delta Adjustment - that compares the entire stock portfolio and gives

• Instructions - Detailed instructions on how to read and enter information.

*** Enter Values into cells that have a WHITE background colour only ***

Video demo not yet available:

By downloading digital products, you agree to join our marketing email list, where you'll receive updates, tips, and exclusive offers. You can unsubscribe at any time.